Employee Benefits

PCORI Fee Guide

PCORI Fee Guide

Applicable Health Plans

Fully insured and self-insured health plans are required to pay the Patient Centered Outcomes Research Institute (PCORI) fee annually by July 31 of the calendar year following the last day of the plan year. When the plan is fully insured, the insurer pays the fee. Plan sponsors1 of self-insured plans are generally responsible for paying the PCORI fee directly to the IRS (along with filing Form 720), regardless of the number of employees (and their spouses and dependents) enrolled in the health plan. Health plans subject to the PCORI fee include:

- Group medical plans (PPO, HMO, EPO, POS or fee-for-service) covering active and/or former employees (i.e., COBRA participants and retiree coverage), and their spouses and dependents

- Grandfathered group health plans

- Retiree-only plans

- Health Reimbursement Arrangements (HRAs)

Plans that provide only excepted benefits2 are not subject to the ACA requirements and, therefore, are not subject to the PCORI fee requirement.

PCORI Fee Amount

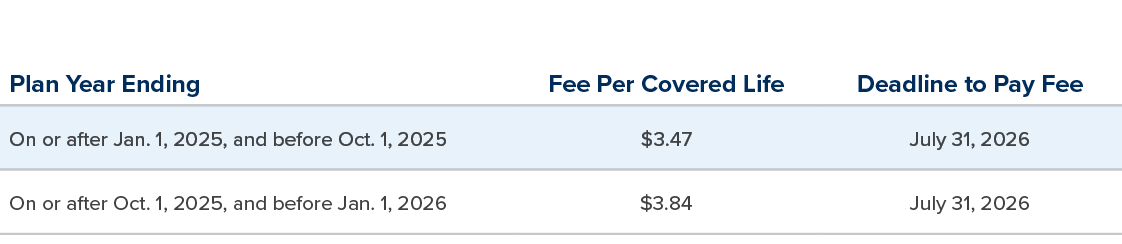

The PCORI fee amount is based on the end date of the plan year, and is adjusted for inflation each year. Although the PCORI fee is based upon the end of the plan year occurring on or after October 1st of each year, for ease of use, this article focuses on only plan years ending in calendar year 2025, which would have a due date for both Form 720 and the payment of the PCORI fee to the IRS by July 31, 2026. The most recent PCORI fee amounts, depending on when a plan year ends during the 2025 calendar year, are described below:

Reporting Covered Lives and Paying the PCORI Fee

The PCORI fee is determined on an annual basis, based on the average number of covered lives enrolled in the health plan during the plan year. The fee is reported on Form 720 for the quarter ending June 30 of the calendar year in which the PCORI fee is being submitted, although the fee is payable for the plan year that ended during the most recently completed calendar year (e.g., the PCORI fee for the plan year that ended in 2025 is due to the IRS by July 31, 2026 and will be reported on IRS Form 720 for the quarter ending June 30, 2026). For plan years ending on or after January 1, 2025, and on or before December 31, 2025, plan sponsors must report and pay the PCORI fee by July 31, 2026. The PCORI fee due July 31, 2026, is $3.47 per covered life for plan years ending on or after January 1, 2025, and on or before September 30, 2025, and increases to $3.84 per covered life for plan years ending on or after October 1, 2025, and on or before December 31, 2025.

Important note: Frequently, we have seen mistakes occur when a plan sponsor either reports the average number of covered lives on Form 720 for an incorrect quarter and/or when the plan sponsor reports the average number of covered lives on the wrong line of Form 720. For example, a plan sponsor may report that the Form 720 is being submitted for the quarter ending December 31, 2025 (which is the date their calendar year plan year ended), rather than properly reporting on the Form 720 that the reporting is being completed for the quarter ending June 30, 2026. These mistakes can mean that the IRS fails to recognize that the PCORI fee was paid for the applicable plan year (which causes the incorrect result of the IRS misapplying the PCORI fee to incorrect years and/or treating the Form 720 and the payment of the tax as being submitted late, which can result in penalties and interest to the plan sponsor). If a demand letter from the IRS is received, the plan sponsor must consult with their tax advisor for assistance with an IRS response. If this error was made for multiple plan years, each applicable Form 720 will require correction.

The average applicable covered lives and the applicable PCORI fee are reflected on line 133 of the IRS Form 720. Lines 133(a) and (b) are reserved for fully insured health plan reporting (which is generally completed by the insurer). A sponsor of an applicable self-insured plan will report average covered lives on line 133(c) for a plan year that ends on or before September 30 of the preceding calendar year. For a plan year that ends on or after October 1 but before December 31 of the prior calendar year, reporting entities should enter the data on line 133(d).

The chart below reflects the correct information to report on Form 720 for plan years ending in 2025, for reference:

Determining Average Covered Lives

The plan sponsor must pay the PCORI fee based on one of the four permissible calculation methods for determining the average number of covered lives under the plan during the year, which must be applied consistently throughout the entire plan year.3 Calculation methods include:

- Actual count method uses the average unique count of employees, spouses and dependents covered by the self-insured health plan on each day of the plan year.

- Snapshot count method uses the average count of

unique employees, spouses and dependents covered

by the health plan measured for an equal number of

days each quarter during the plan year – each date

measured must represent the same month in each

quarter (first, second or third month), and must be within

three days of the measurement date corresponding

with the first quarter. - Snapshot factor method uses the sum of the average number of covered participants with self-only coverage, which is added to the average number of participants with coverage other than self-only coverage times a factor of 2.35 – each date measured must represent the same month in each quarter (first, second or third month), and must be within three days of the measurement date corresponding with the first quarter.

- The Form 5500 method uses the total number of participants covered by the employer’s ERISA health and welfare benefit plan, under which the self insured health plan is a component. The Form 5500 method may only be used for ERISA plans (e.g., not self-insured health plans maintained by a church or governmental entity), and only if the Form 5500 annual return/report is filed prior to the date the PCORI fee is paid.

- For a major medical plan that provides coverage for employees and dependents, the average covered lives equals the sum of the participants covered on the first day of the plan year and the participants covered on the last day of the plan year (i.e., adding the numbers found on lines 5 and 6(d) of Form 5500).

- For a major medical plan that provides coverage to only employees (excluding spouses and dependents), the beginning and end of the year participant counts are averaged (i.e., the two numbers are added together and divided by 2).

Important note: Mistakes frequently occur with the Form 5500 method. Most typically, the error involves using an average of the two numbers when the two numbers should be added, or taking the beginning and end of the year participant counts from an enrollment report from the TPA rather than using the correct line(s) reported on Form 5500 when the health plan is wrapped with other benefits. This can result in underpayment of the PCORI fee.

Determining Average Covered Lives When There Are Multiple Self-Insured Health Arrangements

If the employer offers an HRA (i.e., a self-insured plan) that is integrated with a fully insured medical plan, the plan sponsor (typically the employer) will be responsible for filing and paying the PCORI fee for the HRA. The covered lives calculation for the HRA is based on the average number of employees and former employees covered by the HRA, disregarding other family members whose health care expenses are eligible for reimbursement (even if the HRA may reimburse eligible health care expenses of spouses and dependents).

If the plan sponsor has multiple self-insured health plan arrangements (such as a self-insured PPO and an HRA), only unique covered lives are counted provided the plans have the same plan year. This means that for an HRA that is integrated with a self-insured medical plan, the PCORI fee is based on the average covered lives of employees covered in the employer’s self-insured medical plan (i.e., the employer need not count that life again under the HRA for PCORI fee purposes because that fee is already captured when averaging the number of covered lives in the self-insured medical plan) so long as the HRA and the self-insured medical plan have the same plan year. If applicable, for employee lives that are covered by the HRA but not the self-insured major medical plan, those employee covered lives are added to the average number of lives covered under the self-insured medical plan. Finally, if the HRA and the self insured medical plan have different plan years, then the plan sponsor must take the average number of covered lives participating in the self-insured medical plan, and add that amount to the average number of employees participating in the HRA (disregarding any family members of those employees even if the HRA may reimburse eligible health care expenses of spouses and dependents).

Short Plan Years: The PCORI fee is payable for all plan years that end during the applicable calendar year. This includes short plan years that end in the calendar year that provide coverage during a plan year of less than 12 months4.

Actions Items for Plan Sponsors

Sponsors of self-insured plans should pay close attention to the annual PCORI fee increases and are required to file Form 720 and pay the applicable PCORI fee by July 31 of the calendar year following the end of the plan year.

Plan sponsors who uncover mistakes in reporting should consult with their tax advisors for assistance with the corrective process. This may include filing amended Form 720 excise tax returns for any periods in which errors were made or when providing a response to an IRS demand letter(s).

1 Generally, the entity responsible for reporting is the employer who has established and maintains the health plan for the benefit of its employees and their covered family members. For other types of arrangements (e.g. multiple employer plan established to benefit the employees of multiple employers that are not sufficiently related to constitute a controlled group, and multiemployer plans established by collective bargaining units to benefit their members), the MEWA or the contributing entities may be responsible for reporting.

2 “Excepted benefits” not subject to the PCORI fee include: stop-loss policies, stand-alone dental or vision coverage not integrated with the employer’s medical plan, health FSAs that are only offered to employees who are eligible for the group health plan and the maximum annual reimbursement is limited to the greater of two-times the employee’s annual salary reduction election or the employee’s annual election plus $500, certain EAPs and wellness programs that do not provide coverage for “significant medical care,” certain expatriate plans, and on-site medical clinics

3 See 26 CFR Part 46 Subpart C – Fees on Insured and Self-insured Health Plans

4 Refer to: Patient Centered Outcomes Research Trust Fund fee: Questions and answers (Q&A #12) for more specifics on the application of the PCORI fee to a short plan year.